Rhodium's Dan Rosen on Hiring Me, 30 Years of China-Watching, Decoupling, Debt, Over/Underrated (Track 2 Dialogues and PDFs) + Tweets of the Week

Rhodium's Dan Rosen on Hiring Me, 30 Years of China-Watching, Decoupling, Debt, Over/Underrated (Track 2 Dialogues and PDFs) + Tweets of the Week

Tweets on Xinjiang, Elting Morison, Chairman Rabbit, Forest Sounds, Real Estate Scams, and 2500-Year-Old Beads

The following is a lightly condensed transcript of the most recent ChinaTalk podcast episode.

Jordan: Dan Rosen is the founding partner of the Rhodium Group and leads the China team there. He is also my boss! After nearly a year and a half of working full-time on ChinaTalk, I've finally found a full-time job. Want to tell the story of how we got connected?

Dan: I stuck my head up out of the pandemic foxhole last fall, and I realized that it seemed like half my team was on your show.

And I just said, "I just got to talk to this guy and just see what this little empire is all about." I didn't expect it, but it turned out you were quite well-matched for something that we had been thinking about a long time here.

Jordan: So what happens to ChinaTalk?

Dan: If it weren't for ChinaTalk, I wouldn't have found you in the first place. And if it weren't for my interest in seeing you continue it, you wouldn't be here with me. The problem there is you're going to have to clone yourself if you want to do anything like the quality of output that you've done in ChinaTalk in the past, at the same time you start being the kind of productive Rhodium teammate that I know you're going to be too.

Jordan: Nights and weekends, Dan. Nights and weekends.

Dan: I'm already counting the nights and weekends. Something's got to give! That said, I'm a fan and I'm a convert to the importance of this channel.

Jordan: I just want to say thanks to everyone for supporting the newsletter. Your contributions and occasional consulting projects helped me get through what was professionally a very fallow 2020. And if you hadn’t contributed not just monetarily, but through your forwards and tweets to juice the algorithm to get ChinaTalk in front of Dan, I may not be in this dream position I have today, which is a full-time job with healthcare and benefits, getting paid to spend all day reading and writing about China and technology.

My emotional relationship to the whole ChinaTalk enterprise has been a bit of a rocky one. On the one hand, it's impossible to listen to the show and read this newsletter without realizing that I love this stuff. However, putting so much time into so unlucrative a project, particularly after I had to move back from Beijing to the US, wasn't sustainable.

I've resisted putting podcasts and newsletter additions behind a paywall because I really view this as more of an academic and educational more than a commercial enterprise. I’ve also been hesitant to take positions that would require me to shut down the operation, but that’s a stance I could only have held on to for so long.

I still own this podcast and newsletter, and it will be editorially independent from Rhodium.

Your subscription money will go towards paying the young contributors who have put out some fantastic work of late, as well as for editorial help around podcast editing to free up time to research and record more shows.

I will likely feature more Rhodium analysts in the newsletter and podcast, not because Dan is making me, but because I think they're fantastic people who have interesting things to say about China. Dan, briefly, what is Rhodium and what does it do?

Dan: Rhodium is an independent economic research firm. We're not a think tank. We're a for-profit entity. I spent the first 10 years of my career in the think tank space in DC, the Peterson Institute. Rhodium puts things out there in the marketplace and sees if they had value. We spend a huge amount of our time and effort doing public policy-oriented work and partnership with think tanks still today.

And then we toil to make sure that the public policy thought leadership we invest in and commit to has relevance and applicability in the private sector with corporate clients, financial clients, government clients, folks that have a mission that they've got budget to pursue where we can help. We really are kind of a hybrid that you're signing up for here.

It's super challenging because we've got to both make sure that we have credibility in public policy space, but also relevance in the commercial world at the same time.

Jordan: Why start hiring around technology?

Dan: Of all those areas where we could be looking for people that have more capability than we have in-house, technology is the one that just wouldn't go away. What we don't have without starting to bring people like yourself in is an ability to go all the way down into the weeds and sort out which competing point of view around some very specific debates and issues on tech.

It’s kind of the Rhodium analytic tradition to be able to marry up the macro and the micro in conventional economic analysis around industry, manufacturing, what have you. When it comes to technology, we need to build out the team if we're going to be able to go with our clients and with public interest all the way from on high, but down into the great plains where these debates are playing out.

Jordan: Just like the idea of an ‘America Technology Analyst’ is a silly one, ‘China Tech Analyst’ is also extraordinarily vague and can mean a million different things. Dan and I are trying to work through exactly what would be most relevant and interesting.

If you work at a corporation, investment fund, or government (where people get to vote for their leaders) and have burning analytical questions on China tech, we'd love to hear from you on how we can build up coverage to help you understand what's happening on China and technology. Please do reach out by responding to this email.

So Dan, you’ve in this China economics game a long time now. What do you think have been the phases of analyzing China since you founded Rhodium back in 2003?

Dan: Rhodium since 2003 and professionally since 1993. There’s been multiple generations of Chinese economists who had all the same debates inside China as we've had outside China really.

First, skepticism, even back in the '90s, that China really intended to permit a kind of structural adjustment to totally changed the landscape of the economy. Nobody actually believed that that could happen back when I got started in 1992, 1993. It was probably fair to say people thought it was just going to be sort of window dressing. But over the course of the '90s, we saw like 200,000 state-owned enterprises wound down, combined with others, shut. Corporatized was the term back then.

Privatized was still not approved verbiage, if we're talking about that. We saw the number of goods that were bought and sold at market prices go from low double digits to over 90% of all transactions in the marketplace being sold and priced according to supply and demand. Those were pretty radical validations that there was something different happening here than the more cynical, more real politic folks who thought that the leadership wasn't really going to let the market off a leash.

By 1998, '99, it was clear that it was being led off the leash, and that was interesting. Economists inside and outside China took a while to catch up to that. But after WTO session in December 2001 is when it finally formally happened, the whole party moved over to that side of the boat. And just as they did, of course, economists always being a lagging indicator, I'm afraid to say because they deal with data, which describes what happened yesterday by definition most of the time, that impulse to make the market more central started to show some limits. And in the first half of the decade after 2001, that was sort of ambiguous, mixed signals. A lot of ways to say, "Well, of course, it's just sort of a slight corrective back in the other direction to balance things out."

By the end of the decade to the 2000s after the global financial crisis, et cetera, it was sort of a full-blown shift back to doubt as to whether the Chinese economy would continue to marketize. I think looking at the whole arc of almost three decades now, that has been the most fundamental dynamic that I've seen in analysis.

This sort of lagged awareness that marketization wasn't smoke and mirrors. It was real, but then also a lagged and begrudging acknowledgment that our assumptions that would keep going to a certain end point were flawed to some great extent. And now today we're right in the middle of this extraordinary debate about whether things could even possibly go back in a more liberal direction again, I would say.

Jordan: You talked about people being surprised at marketization being a thing that actually happened. The other inflection point we've seen, of course, in the past five years is political liberalization going into reverse. What was it like watching China when people were optimistic about the future of where the CCP was heading and how was that for you seeing that turn with the rise of Xi?

Dan: I guess I would say, Jordan, just stick around a little bit and you'll have a chance to see for yourself. Another way to put that would be that a China pessimist is just an optimist who hasn't hit the bottom of a cycle yet. Look,

China made its way down a liberalizing path not because it was forced to do so by the United States or anybody else, but because its very hard-headed leaders a long time ago came to the conclusion that that was the only way to make China great again.

It worked by allowing a lot of apolitical, practical, hardworking Chinese people off silly ideological nationalistic leashes. A tremendous amount of growth and dynamism and potential was opened up and reshaped the destiny of the country. Looking even more recently, I guess I would take a slightly contrarian view even though the Xi Jinping era. I think Xi Jinping coming in 2012, '13, the most really notable thing about his start is that he puts somebody like Liu He in charge of crafting economic strategy.

And the first economic planning manifesto put on the table in November 2013 is notable not for its illiberalism, but for the clarion call to move to the next stage of economic reform. And that wasn't just dogma on a piece of paper. From 2013 until 2016 and '17, you had maybe half a dozen really serious first order efforts to take the next lap around the track in terms of economic opening up. You had an attempt to rein in the shadow banking market in 2013. You had an opening up of the financial account for capital outflows in 2015.

You had a release of the equity markets allowing them to bubble up in 2015-2016. You had an attempt to de-leverage the financial system in 2017-2018. You had an attempt to internationalize the renminbi, even though everyone understood that meant you were going to have to stop manipulating the currency the same way as had been done in the past. These were not all sort of gimmicks or prestidigitation [ed: yes, it’s a word, “the process of doing a magic trick by hand”].

These were actually real serious reforms, and we know they're real because each one of them created a miniature crisis that had the potential to cause a much more serious crisis in the system so much so that they had to reverse course and go back to a more lockdown approach to dealing with that set of policies, right?

Even now there's reason to be optimistic if you want to be, but to be fair and to be practical, we have to look at the other side of the ledger and all the things that are happening simultaneous and parallel to that effort that are distinctly illiberal and attempting to put stability over all else, right? It's trying to have dynamism and stability at the same time. You tell me how that works.

Jordan: I was supposed to answer that question?

Dan: Yeah, good luck. It's your first job assignment! Memo next Tuesday please.

The Decoupling Dance

Jordan: Moving on…decoupling! Rhodium recently put out a report with the US Chamber of Commerce you co-authored with Lauren Gloudeman trying to put numbers around what a hard decoupling would mean. What are your takeaways from that exercise?

Dan: Decoupling, it's a fraught term. We're going to probably have to throw it overboard along with like the Washington consensus. It's got too much baggage on it already, but we actually started talking about it seriously about three years ago after the December 2017 new national security strategy, which made it clear to us that engagement as we knew it was not just being tactically set aside by a Trump administration looking for a deal, but was a real trend.

Partial decoupling…is kind of natural, right? Two countries that are like-minded are going to be more interoperable, say Canada and the U.S., Than two countries that are systemically not like-minded. No matter what you think about China and the Chinese economy, there's no pretending that it's the same kind of economic bedrock assumptions about the role of government, the role of the market that we have in the United States.

All that engagement policy over the decades was contingent, predicated on the working assumption that China intended to converge with the advanced economy like liberal economic systems. In the past couple of years, China has made it clear that if it did in the past, it doesn't presently intend to fully converge. We have to do is stock-taking of the ways we are engaged, the way we had anticipatorily started to lower barriers to economic interaction and go ahead and open all these channels up.

Some amount of partial decoupling is a reality. It doesn't have to be put in war-like terms. It's just the reality that not all systems are exactly alike, and thus, they can't be equally open to one another as they would be if they were exactly alike. We now then have the tough analytic question of what's that going to cost.

If you're going to not just talk about resizing the extent of our engagement, but actually do something about it, there are going to be winners and losers. There's going to be a price tag. Because China and the United States are the two largest economies in the world, it's going to be a big price tag. And yet the initial forays at re-engineering our interaction from the past couple of years were done without having much of a sort of economic impact assessment if you will. Lauren and I set out with the chamber to do a stock-taking of that.

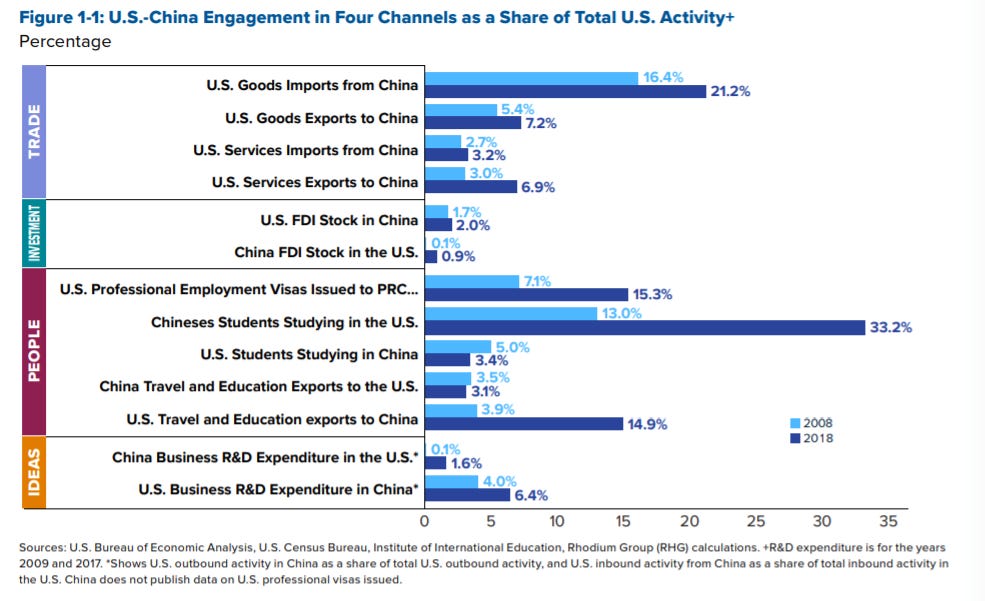

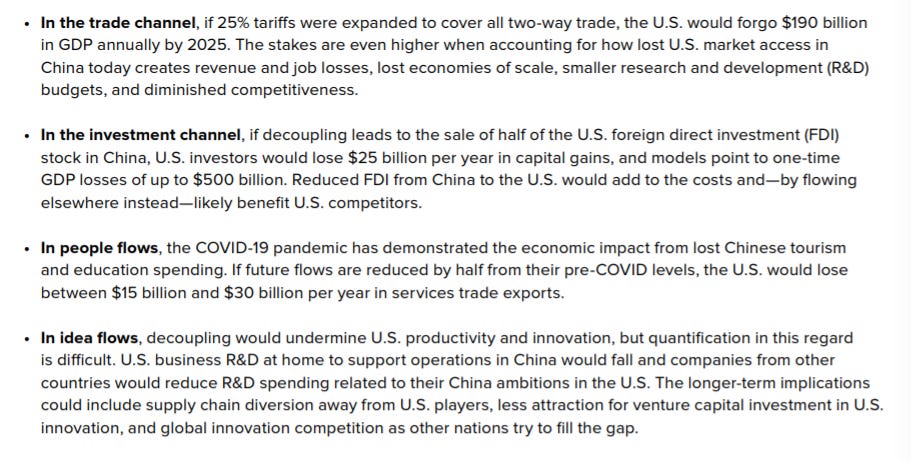

We put out a study that offered a broad order of magnitude understanding of what decoupling would mean in four channels, trade finance, people flows, and technology and ideas flows.

There's no kind of decoupling that doesn’t have a price tag in the hundreds of billions of dollars for the United States.

Does that mean that we should shy away from it? Not necessarily! It all depends on whether we're really buying a security benefit or some kind of long-term economic strategic benefit by changing how we work with China. But we have to do the math because the price tag is too big just to throw our credit card down without looking at the check.

How to Do Industrial Policy Right

Jordan: We've seen it in the past few months the Biden administration, as well as folks on the Hill warming to industrial policy. You have Biden talking about a cool $37 billion for the domestic chip industry, but also a line you often hear out of DC that “the U.S. doesn't want to out China China.” What are lessons to be learned applicable to U.S. policy-making from Chinese industrial policy and the State's role in the economy? And what lessons should we be sure not to learn?

Dan: It's such an important question, right? We definitely don't want to try to ‘out China China’ for two reasons I'll offer. First, us trying to outdo China is not going to work. We are not set up like China. We don't have the kind of one party command and control structure that China has on paper that allows it on paper to do all this industrial policy stuff. We simply cannot do it that way.

We have a democratic society where the people who need to pay the taxes that fund industrial policy have a say over whether we conclude that we should provide massive subsidies to businesses who it turns out might make investments anyway without the subsidies. We've got a different kind of system, and we can't do it the Chinese way.

The second reason not to do it the Chinese way is it the Chinese way actually doesn't work as well as the Chinese leadership itself likes to suggest it works.

If you look at not just the volume of money and resources and effort that China has put toward things like industrial policy, particular industries, particular firms, but ask how much have they actually gotten for that in terms of real innovation, and how much debt has built up that's borrowed from the future, I think it's not at all clear that Chinese industrial policy is worth emulating, even if we could. In fact, I'm pretty much ready to say it should be avoided by not just the United States, but virtually all countries.

Chinese Debt

Jordan: So talking about debt, Dan, China in 2020 was the only large economy with a positive growth rate. But at the same time, we've seen a slow but steady drumbeat of credit events from nationalizations and bank restructurings to street protests outside financial firms, headquarters, literal bank runs of people lining outside of their bank and folks in the bank, throwing money in the window just to make sure that people realize there's still cash available. What should folks make of the fact that we see these two trends happening at once?

Dan: For starters, both stories are true, right? China did turn in a better short-term performance than anybody else in 2020, and it did so because the center has the ability to reach in and compel the financial system to behave in various ways, right? That's a great solution to the short-term problem of how to deliver more growth in the near term.

The problem is that you can only get away with that year after year if you have credibility if the center has the credible ability to say that this is going to create more and better growth in the future, we're going to have a good return on investment, in other words, right? We've been doing a project for five years now we call China Dashboard looking at this question of, what is the return on all this debt that China incurs?

When Xi Jinping took over, for every about three and a half or four renminbi of new debt created every year, there was about one renminbi of persistent growth in GDP and output in the economy and the nation. And that was pretty close to international standard, like what we considered to be a pretty good international ratio. Today it's nine. You need nine renminbi of new credit to be issued by somebody to get that same one renminbi of GDP growth out into the future.

Something is not going in the right direction and that's not just a normal sign of a country reaching middle-income levels. In fact, quite the opposite. At this level, you can start to see financial efficiency go up because some of the early stage maybe not great rate of return but socially very valuable investments, that stuff should be done after 40 years of five-year plan after five-year plan after five-year plan. Now we should start to see, nationally speaking, a better financial system with better returns on investment, but we're seeing the opposite.

It's not to say that the party doesn't have the power to reach in and tell the banks what to do for a couple more years, throw that money in the window as you put it, which is literally true. That does happen, right? But it's less and less credible to believe that there's a smooth way from doing it this way to doing it the way that efficient market economies do it. And that's going to have to be addressed and it's not being addressed yet. [for more on this, check out my interview with Lauren and Logan of Rhodium from late last year on ‘The Chinese Financial Crisis That Never Happened’]

Overrated/Underrated: Track Two Dialogues, Talking With Policymakers, and Enormous PDFs

Jordan: Dan, track two dialogues. Are you wasting your time?

Dan: Oh no. You're starting to sound like my other colleagues already, second guessing whether it's a good use of a partner's time to do all these dialogues…I see I'm going to have to take you out to lunch or buy you a good bottle of wine or something to bring you over to my side. I think track two dialogues very much can have tremendous value and play an important role.

Track two dialogues are people who at some point have had a chance to be in government meetings with their colleagues from the other side and talking about things that are too impolitic or inappropriate for people in the official sector to be talking about. You can trial balloon things. You can test out some ideas. When they're done well, they play a crucial role. Everybody has different opinions about what makes them run well, and also lately it seems like everybody...

Jordan: Well, what's your opinion on what makes them work well?

Dan: First of all, there's like a skill in them. Everybody who wants to raise money for their think tank just announces that they're going to do a track two dialogue. That in my estimation does not really make it a meaningful track two dialogue. I'm kind of conservative and stodgy about this, I guess, in my old age here. But to me, they work best when they flow from an actual ask from the official sector, from the track one world.

If somebody in track one says, "We'd like to better understand if it's possible to make some progress on this issue," the two sides are finding it too politically scary to get together right now and talk about this officially. They don't trust each other enough maybe. Why don't you put together a gathering of former senior officials or something like that and see if you can get a little bit of sense of whether we can take a few more chances here, what the other side would say.

That means that this is not just people getting paid by the word to talk, but there's actually a mission and a purpose and an objective to test something out, explore some ideas, and crucially bring it back to a ready audience that is interested in what the results are. If folks just say, "I'm going to do a track two dialogue. We're just going to get together, and then we're going to publish an open letter of what we think the world should be like," I mean, that's fine. It's great that civil society does that. It's important. It's crucial, but it's not what I would call an effective track two dialogue mode.

Jordan: Conversations with policymakers in government sitting in either the private sector or in a think tank, how much of this is them reaching out for our genuine request for advice or versus them sort of working the empires?

Dan: It's a savvy question because a lot of it is the latter, a lot of it is persuasion by other means, right? Inviting folks in to have a conversation, dangle a little bit of information, but what you're really doing is influencing the debate and trying to massage where the conversation is going and all of that.

There is a tremendous amount of that that goes on, and there is, I think, a tremendous amount of naivete on both sides, Americans talking to their own officials and to Chinese and also Chinese talking to their own and to focus on abroad oftentimes under-appreciate how much this is sort of a narrative management exercise more than government people really asking for inputs and opinion.

That all said, there always is a channel and room for some really important, open-minded, probing interaction between people who are in government and people who have time to think, right? As you put it a minute ago, you're getting paid to write and think about China. That is true and that will continue until the point where there's no value in what you produce, at which point you'll cease to be paid. Then we’ll all have to fold the firm, right?

The acid test of whether what we're doing is sustainable is whether people who are in government and don't have time to do any thinking for themselves are interested in talking to us to catch up on what's happening and figure out what is going to be important for them to focus on next. There are both of these things.

There's a lot of narrative management stuff that happens, and then there is also absolutely room for crucial dialogue and interaction between people in the private research sector that we're in and people in government.

Jordan: So speaking of making things that people will read in government, report length. I just came across the National Security Commission on Artificial Intelligence's 750 page PDF, which I will make my way through at some point…Dan, what is the right length for a report?

Dan: When I started out in the '90s, the first book I wrote called Behind The Open Door. And at that point, 1996-'97, that was essential for me to demonstrate my credibility, right?

There's a time and a place for doing longer format work to really work through and evaluate every possible nook and cranny of an issue. But in the policy space and when you’re dealing with the C-suite of companies, you just have to boil it down and put it into a shorter format because people just don't have the time.

We used to think that a proposal was better if it offered more length, but a 10 page memo is much harder and better to write than a 50 page memo.

Jordan: In a different media world, I would have spent the past two and a half years writing a book instead of writing a newsletter. And this is something that my parents kept telling me, "Jordan, when are you going to write your book? When are you going to write your book?" On the one hand, I'm insecure that I don't have some academic press book to my name. But at the same time, I feel like there really is a lot of value in trying to mix up... I don't know. I’m going to write that book at some point.

I don't think long research is unfounded, but there really is something in being able to write short and impactful.

Dan: Is there an analog in the podcast space? Is there like a certain time for an episode beyond which it's like indulgent to expect people to stick around?

Jordan: That's a good question. There are shows that are two, three hours and I think they're fine. What matters most is the quality really, not necessarily the length. I run anywhere between 45 minutes and an hour and a half because I feel like guests tend to lose stamina once they pass the hour-long mark. I do think doing a one-on-one interview for 10 minutes or 20 minutes, you leave a lot on the table.

Dan: I guess I'd say the same about books, right? I mean, the simple reality of life is that people don't have time to read five 300-page books a week. They will make time to read 15 five-page policy briefs, right? But there are some things that need a book-length treatment because they're just that big a topic. In a given year, Rhodium will put out probably three or four, if not five studies.

The length of the cost of decoupling study from the chamber you mentioned to the original two-way street, tracking of foreign direct investment, these things we're pushing 80, 90, a hundred pages. There's still room for that book, tell your parents not to give up hope.

China Twitter Tweets of the Week

A thread. What else should I read on this theme?

Thread

Thread

Super relaxing, I highly recommend

Eastern Zhou Dynasty beads from 500BC!

Congrats on the job!